INTRODUCTION

Every organisation is required to implement management accounting system to manage the organisational activities in optimum manner. It is not compulsory to implement these systems within the organisation but necessary to record, analyse and improve existing performance of different departments of organisation. The concept of management accounting is used by the internal parties to enhance their decision making and bring coordination among the different organisational activities which perform on daily basis to achieve common objectives. Application of the provisions of different management accounting systems helps the manager of organisation is to perform necessary functions within the organisation related to planning, organising, monitoring and controlling. There are large number of advantages which are gathered by the organisation such as high market share, high number of profitability, higher involvement of employees, optimum utilisation of resources and timely completion of objectives within stipulated period of time. Zylla is manufacturing organisation which deals in diversified projects (Cadez and Guilding, 2012V).

In the present assignment report explain about different types of management accounting systems along with their essential requirements within the organisation and different types of management accounting reports and their importance which are gathered by the organisation. Also, application of the marginal and absorption costing regarding formulation of income statements, advantages and disadvantages which are associated with different types of planning tools used for the purpose of budgetary control and contribution of management accounting systems to respond financial issues.

Increase Your Odds of Success With Our

- Scholastic academic documents

- Pocket friendly prices

- Assured reliability, authenticity & excellence

TASK 1

P1: Different types of management accounting and its essential use

Management accounting: It is a concept which includes the process about collection, interpretation, analysis, recording of important information related to organisation to take accurate and reliable decisions which contributes in achievement of desired objectives. Use of these systems helps to collect statistical and financial information through day to day activities are performed precision within the organisation. The different system is used regarding controlling of the different departmental activity in the organisation and improvement of their performance through finding out the deviations. It helps to design more appropriate solution which contributes in reduction in the amount of risk and deviations in actual performances. The different type of management accounting systems which are considered as the important part of the organisation as current market scenario includes inventory management system, job costing system, cost accounting system, price optimisation system etc. On the basis of such various kind of information budgets are prepared which are needed to follow by the employees to optimally utilise their given resources to accomplish their desired targets.

Essential requirements of management accounting

Management accounting is the integral part of every organisation which is required to adopt for improvement of the understanding between employees of organisation regarding each other’s work. It provides the opportunity to the management of Zyalla Company is to ascertain their full support and create positive environment within the organisation. It helps to create good communication through which strong teams are build in Zyalla which able to perform difficult tasks. The different requirements which are fulfilled through its implementation within Zyalla is defined below:

Optimum utilisation of resources: One of the important aspect for organisation is to optimally utilise their given resources to attain maximum returns. In this regard, inventory management system plays an important to effectively manage the level of stock within the organisation and allocate it to operational department as per their requirements. It helps to operate at their maximum capabilities and convert the raw material into final goods of effective quality through different requirements of customers are fulfilled (Fullerton, Kennedy and Widener, 2013).

Risk management: Another important function which performed with the helps of the use of the provisions of management accounting systems is to assess the future risks which are associated with their operational activities through preparation of different strategies.

Appraisal of performance: The different information which is collected with the help of this system is used further in the preparation of budgets which are work as standards. It is used by the manager of Zyalla to appraise the actual performance of employee and departments through comparison to such standards. The deviations are removed through provide effective direction. It contributes in accomplishment of objectives.

Different types of management accounting systems

There are many type of management accounting systems which are required to implement by the manager of Zyalla to attain competency in their business operations. So, different kind of systems and their functions within Zyalla are defined below:

Cost accounting system: The main function of this system is to manage the cost of their products through reduction in the amount of unnecessary expenses. It helps the organisation to attain competitive advantage in market through providing the products at low cost with high profit margin. This system used to continuous monitoring over the costs of various aspects which involved in the process of production of product to become cost efficient in appropriate manner.

Inventory management system: The main role of this system within Zyalla is to effectively manage the stock of organisation. This will improves their decision regarding ordering of the right quantity of order through use of EOQ system for effective utilisation of their resources. This will also provides the opportunity is to effectively allocate the stock to high number of benefits regarding improvement of their production capacity to meet the demands of customers.

Job costing system: It is important management accounting system which is important for manufacturing organisation which produces multiple products. It is most suitable for Zylla because it manufactures diversified products. The main function of this system is about allocation of cost to each and every item which is used in the production process. It assists the manager of organisation to track their expenses to make the organisation more profitable (Luft and Shields, 2010).

Price optimisation system: It is effective system which is used by the management of organisation to fix the price of their different products. This provides the opportunity to the manager of Zyalla is to identify the impact of different pricing level over the buying behaviour of customers. Through such analysis right price of their products is selected through which they are able to attract the large number of customer and improve their sales.

P2: Different methods for management accounting reporting

Report is a document which contains the different information which is further used to interpret important results through application of the different methods. There are many types of management accounting reports which are required to formulate by the management of Zyalla to bring effectiveness in their operations. These reports are prepared with the help of information which is gathered from the application of systems. The different kind of reports along with their functioning in Zyalla is defined below:

Accounts receivable report: One of the important report required to prepare by the manager of Zyalla to maintain liquidity with the organisation. This report provides the information about the outstanding amount which is due from debtors. To make the report more effective need to segmented their invoices on the basis of the time period to which they are due. It helps bring changes in their credit policies as per requirements to timely collect their debts.

Inventory management system: This system provides the information about the level of stock which is present in organisation and how much is required over specific period of time to meet the demands of customers. The techniques which are used in this regard include ABC and Just in time.

Job costing report: Formulation of this report is necessary for Zyalla to ascertain the information about the most profitable aspect or product of organisation where need to provide give more emphasis. This will also enhance decision making regarding provide les effort to least profitable aspects to save their extra cost.

Importance of management accounting reports

There are benefits are gathered by the management of Zyalla through preparation of these different kind of reports which are defined below:

Effective control: These reports are proved s the effective tool for controlling different aspects in appropriate manner. It also assists in the process of monitoring which reduce the chance of mistakes. It contributes to enhance the performance of employees.

High profit generation: Formulation of job cost report helps to provide more efforts to profitable aspects which help to earn more amounts of profits. Also, inventory reports provide the opportunity about optimum utilisation of their given resources which enhance profitability.

M1: Benefits of management accounting:

There are different type of benefits are achieved by organisation from application of management accounting systems are defined below:

Job costing system

- It helps in estimation of all type of costs which are incurred by organisation in the process of manufacturing.

- It helps in prevention of duplication of work

Price optimisation system

- It helps in ascertainment of attitude of customers towards different prices of products

- It helps in maximisation of operating profit of company

D1. How management accounting systems and accounting reporting is integrated within business

The integration between management accounting reports and organisational process is understood from the points which are defined below:

|

Type of reporting |

Integration with organisational process |

|

Budgeting reports |

Integration between organisational process and budgeting reports helps to improve concentration of targeted results |

|

Accounts receivable report |

It helps the management of organisation in creation of better collection policies |

TASK 2

P3: Various costing methods

Cost: It is an amount which spend by the organisation to produce something new and valuable which has new features. It can be referred as the product which is manufactured by the organisation and paid some amount of money to get it in actual and final form. So, the total cost of product includes the amount of all the aspects which contributed their efforts in the process of production. Such different items whose amount is the total cost of the product is included is defined below:

- Raw materials

- Labour

- Efforts

- Opportunity cost

- Risk

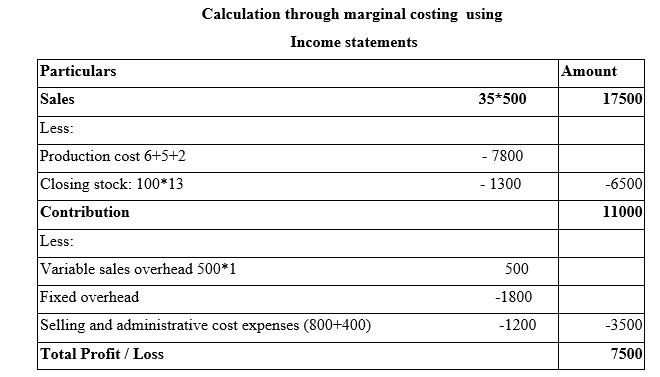

Marginal costing: It is also known as variable costing method because only variable costs are considered while calculating the cost of product. This method helps to analyse the impact of change in the cost due to increase or decrease in the units of production. It is mainly used by the manager of organisation to make their short term decisions.

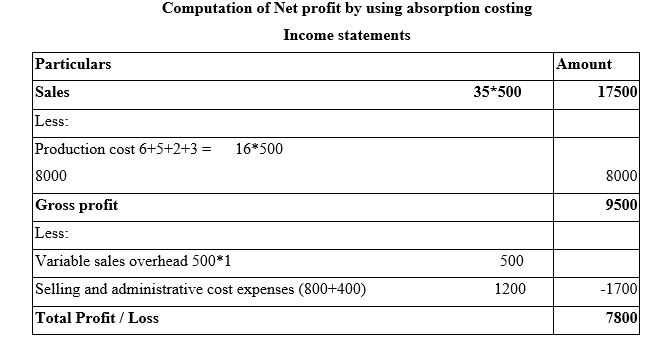

Absorption costing: It is also called as full costing method where both fixed and variable costs are considered. It assists the manager to take long term decision makings.

M2: Evaluation of accounting techniques

The basic purpose behind the use of accounting tools is about collection important internal information information regarding organisational functions. This will improves the decision-making of management and helps in adoption of most profitable project. From assessment of operations of company identified that having good position in market which enable them to easily expand their operations in future.

D2. Financial reports that accurately apply and interpret data for a range of business activity

For interpretation of organisation profit two different methods are used absorption and marginal costing method. The amount of profit which is ascertained by company from use of absorption costing method is 7800. From use of marginal costing method the amount of profit attained by organisation is 7500. the different in amount of profit of 300 is noticed due to non involvement of amount of fixed cost in marginal costing method. (Van der Stede, 2011).

TASK 3

P4: Advantages and disadvantage of using planning tools

Budget: It is one of the viable methods by which chiefs can assessed its aggregate expenses and costs which will cause by organization. It is very much arranged and efficient gathering of records for a particular timeframe. It is an entire system of activity and making arrangements for a specific target. Fundamentally, it is set up for greatest of five years. It can likewise be taken after if comes about are not in considerable.

Budgetary control: It alludes to be a compelling system which is utilized as a part of operational exercises, for example, arranging, sorting out and controlling exhibitions of an association. In this genuine pay and general going through are broke down with arranged pay. It is required to be taken after with certain procedure keeping in mind the end goal to keep up legitimate adjust.

Process of budgetary control

- Research with concern administrators: It is an imperative step for supervisors to make legitimate assessment about spending prerequisites in an association. Financial plan are made subsequent to counselling it with each division.

- Determination of successful supposition: Subsequent to social occasion data from all offices, for example, fund, HR and activities. A supposition is made about techniques for future conjecture.

- Set hierarchical information for spending plan to accomplish objectives: In this procedure, a well sort out rundown of detail data is set up by amassing of information which are gathered from office. An objective is set by keeping future results in the psyches.

Measurement of data with real: The situation of Zylla organization is estimated through utilizing genuine data as per the standard one. By this correct aftereffect of execution can be resolved (Vaivio and Sirén, 2010).

- Review investigation: It is the last stage under budgetary control. Chiefs can look that above disclose steps should be break down before making it vigorously.

Planning tools: In each association, arranging alludes to be organization devices which is related with vision of the organization up and coming way. There are some particular kinds of instruments which are utilized to control spending plans. For example,

Forecasting tools: It depends on presumption which depends on inner control administration that comprises of powerful abilities, learning and basic leadership. It remain depends on authentic information for the goals of assessing future targets. To make look into about the changed mechanical controls that gives data with respect to various critical viewpoints. Such figure enables the administration of organization to comprehend about industry patterns and the potential happenings which are happen in the market like requests, costs and work. Under this gauge, they need to look another imperative component like buyer conduct, propel innovations, methodologies embrace by retailers and producers, enactment and condition of economy. This aides in ID of future elements which have long haul effect on business tasks. As per inquire about, chief has capacity to make arrangements and spending plans and guide their capacities towards accomplishment of authoritative goals.

Favourable circumstances: It is essential for ventures with a specific end goal to inspect pre-set targets. With this, directors can assess add up to cost and deals volume they are caused in organization future.

Impediment: At times, it isn't taken as fundamental instrument as estimating is completely in light of presumption. It is hard to appraise add up to costs or costs Zylla organization will get.

Scenario analysis tools: By the utilization of this instruments, administrators can respond their reaction as pre the present pattern in advertise. It helps to arranging, operational and contributing organization of Zylla organization. It changes of as per varieties popular in the market (Quinn, 2014).

Focal points: with the assistance of situation device, directors of the organization can create appropriate thought in regards to there determination and up-coming open doors those are constantly dubious for them.

Weakness: It considered that arranging instruments which is framed for distinguishing proof of a company's basic leadership at basic circumstances. Actualizing an alternate course of action can simply successful in acquiring adequate measure of outcomes.

Contingency planning tools: this is one of the important planning tool which helps to demonstrate the budgetary control process in effective and perfect manner. contingent instruments which is encircled for recognizing proof of an organization's essential authority at fundamental conditions. Realizing a substitute strategy can essentially fruitful in securing satisfactory measure of result.

Advantages: it helps to sort out the complex business situations and the contingent situations of organisation. It is critical for restricting cost so extra weight can be supervised.

Disadvantage: this planning tool also do not provide accurate information and data in respect of future plans and estimations. More over this information remain associated with forecasting contingent situations which also remain undecided.

M3 Assessment of arranging apparatuses

Basically planning tools are used by the organisation for the purpose of setting standards. The tools which are used in this regard includes forecasting and scenario. Some disadvantages are attached with use of these tools like not necessary to provided information is correct always.

D3 Basic examination of monetary issue

The basic issue faced by organisation is related to funds. This will have direct negative impact upon their productivity. Analysis of such issues at early stage helps in reduction amount of future risks. (Tucker and Lowe, 2014).

TASK 4

P5: Different measures to determine money related issues

It has been discovered that each association is working for some thought process. In any case, they are not ready to came to their objectives on account of money related issues connected with it. There are such a significant number of issues which are displayed in an association. It is related with operational, contributing and budgetary viewpoints. These issues are create through utilization of obsolete advances. Some of them are:

Productivity: There are a few issues which are available with benefit those are connected with Zylla organization. It can build additional cost and weight on them to reach at there goal.

Cost wastefulness: Couple of issues are exist with generation procedure of items and administrations. It is emerging in view of wrong utilization of cost bookkeeping framework.

Execution control and administration: It is connected with budgetary position of organization amid the time. With the not assessing execution of organization in amend way it will make fumble of activities (Otley and Emmanuel, 2013).

With a specific end goal to conquer the above money related issues directors would us be able to following methods those are examined underneath:

KPI: Key execution pointers is said to be one of the pivotal instruments which is utilized to solve money related issues by contrasting information of organization. It ought to be of at various times year premise. With this, execution of every single one working in an association can be assessed.

Benchmarking: It is the way toward surveying the execution of an association's products and Enterprises or procedures against another firm accept to be the best in the business. This instrument is utilized by the administration of the firm all together decides the internal open doors for the change of firm execution. In any case, this can be said that there are basically two normal sorts of change openings which are: general and sensational. The standard change is incremental, covering just little courses of action to procure sizeable advances. While, emotional change is just risen by means of re-designing the whole inner work process.

Contrast between two organizations

|

Unicorn Grocery |

Zylla Company |

|

As per this, as they are working at wide scale so they require culminate checking framework so issues can oversee adequately. |

Under this, as organization is working at a little level so they have to control their operational exercises in well compose way. |

|

KPI and benchmarking can be the ideal alternative for this organization. |

SMART apparatuses are required to be used in more viable and in more critical circumstances. |

M4: Assessment of budgetary issues

The basic tools which are used for the purpose of resolving financial issues includes KPI and Benchmarking. This helps in fixing of standards and continuous watch upon performances. This will helps in removal of issues through improvement of skills of employees.(Morales and Lambert, 2013).

Set in Motion the Plan for Exemplary Grades with Our Extensive Academic Writing Services

Premium Assignment Services

CONCLUSION

From the above venture report, it has been inferred that administration bookkeeping is a fundamental angle for Zylla organization with a specific end goal to supervisor there every day tasks. The task brings a total feature of organizations exhibitions through utilizing bookkeeping and announcing framework. With the end goal of look at net gainfulness certain costing techniques can be used. Some arranging apparatuses are talked about under this venture keeping in mind the end goal to control spending plans. The comprehension of money related issues and important measure to settle those are clarified obviously.

You may also like to read: Unit 5 Management Accounting Assignment Help H/508/0489

REFERENCES

- Vasile, E. and Man, M., 2012. Current dimension of environmental management accounting. Procedia-Social and Behavioral Sciences. 62. pp.566-570.

- Van der Stede, W.A., 2011. Management accounting research in the wake of the crisis: some reflections. European Accounting Review. 20(4). pp.605-623.

- Vaivio, J and Sirén, A., 2010. Insights into method triangulation and “paradigms” in interpretive management accounting research. Management Accounting Research. 21.(2). pp.130-141.

- Quinn, M., 2014. Stability and change in management accounting over time—A century or so of evidence from Guinness. Management Accounting Research. 25(1). pp.76-92.

- Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and relevance. Critical perspectives on accounting. 23(1). pp.54-70.

- Tucker, B and D. Lowe, A., 2014. Practitioners are from Mars; academics are from Venus? An investigation of the research-practice gap in management accounting. Accounting, Auditing & Accountability Journal. 27(3). pp.394-425.

- Otley, D and Emmanuel, K. M. C., 2013. Readings in accounting for management control. Springer.

- Morales, J and Lambert, C., 2013. Dirty work and the construction of identity. An ethnographic study of management accounting practices. Accounting, Organizations and Society. 38(3). pp.228-244.

- Luft, J and Shields, M.D., 2010. Psychology models of management accounting. Foundations and Trends® in Accounting. 4(3–4). pp.199-345.

- Herzig and et. al. 2012. Environmental management accounting: case studies of South-East Asian Companies. Routledge.

- Fullerton, R.R., Kennedy, F.A and Widener, S.K., 2013. Management accounting and control practices in a lean manufacturing environment. Accounting, Organizations and Society. 38(1). pp.50-71.

- Cadez, S and Guilding, C., 2012. Strategy, strategic management accounting and performance: a configurational analysis. Industrial Management & Data Systems. 112(3). pp.484-501.

- Boyns, T. and Edwards, J.R., 2013. A history of management accounting: The British experience(Vol. 12). Routledge.

- Arroyo, P., 2012. Management accounting change and sustainability: an institutional approach. Journal of Accounting & Organizational Change. 8(3). pp.286-309.

UPTO50%

Avail The Benefit Today!

To View this & another 50000+ free